My newsletter readers got a sneak peek at some of this content over the summer when recession bells first started ringing. If you’d like to join the best group of monthly-ish newsletter readers on the internet, sign up here.

For months now it feels like we’ve been teetering on the knife’s edge of a big question:

are we headed for a recession, or nah?

If your first thought is “wait, how would I know?”… first of all, that’s an entirely reasonable response. An economic recession isn’t super well-defined, which is why the talking heads and op-eds all get paid to fight about it; there isn’t a team running around pinning scarlet R’s on world leaders when their economies cross an invisible threshold (that I know of).

The dictionary definition of recession is: “a period of temporary economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters.” Investopedia goes a bit further, saying the decline is “significant, pervasive, and persistent,” and also include “declines in economic output, consumer demand, and employment.” Woof.

I was an official-recession naysayer for a little while because so many things about the economy were still objectively solid, but as time goes on, it looks like we’re maybe barely there; the US GDP dropped a smidge in each of the first two quarters of 2022 (the US GDP advance estimate comes out next week on October 27, just in time for Halloween frights). It’s starting to look like we’re trick-or-treating at the door of the Big R (although a few better-than-expected Q3 earnings reports are peeking out through the curtains, so maybe not quite?). But does it actually matter to you if we’re “officially” in a recession?

Probably not!

Whether or not the US has a DTR (“defining the recession”) chat in time to make it official before the holidays, you might still be unhappy in your personal relationship with the economy. Thanks to major inflation (a.k.a. price increases) and interest rate hikes hitting Americans right in the wallet, the vibes have been off for awhile. The markets are a terrifying rollercoaster ride for anyone who regularly checks their investment account balances (stop doing that if it stresses you out! please!). And so far, the Fed’s interest increases haven’t done much to cool things off.

Part of the problem is that the job market is still very tight, meaning that there are more job openings than workers to fill them, and unemployment claims are still quite low. The Fed is supposed to both keep inflation low and make sure people are maximally employed; although the Fed doesn’t want anyone to wind up out of a job (their mandate is the opposite!), the fact that jobs are still tight seems to signal that there’s some room to maneuver in their fight against inflation.

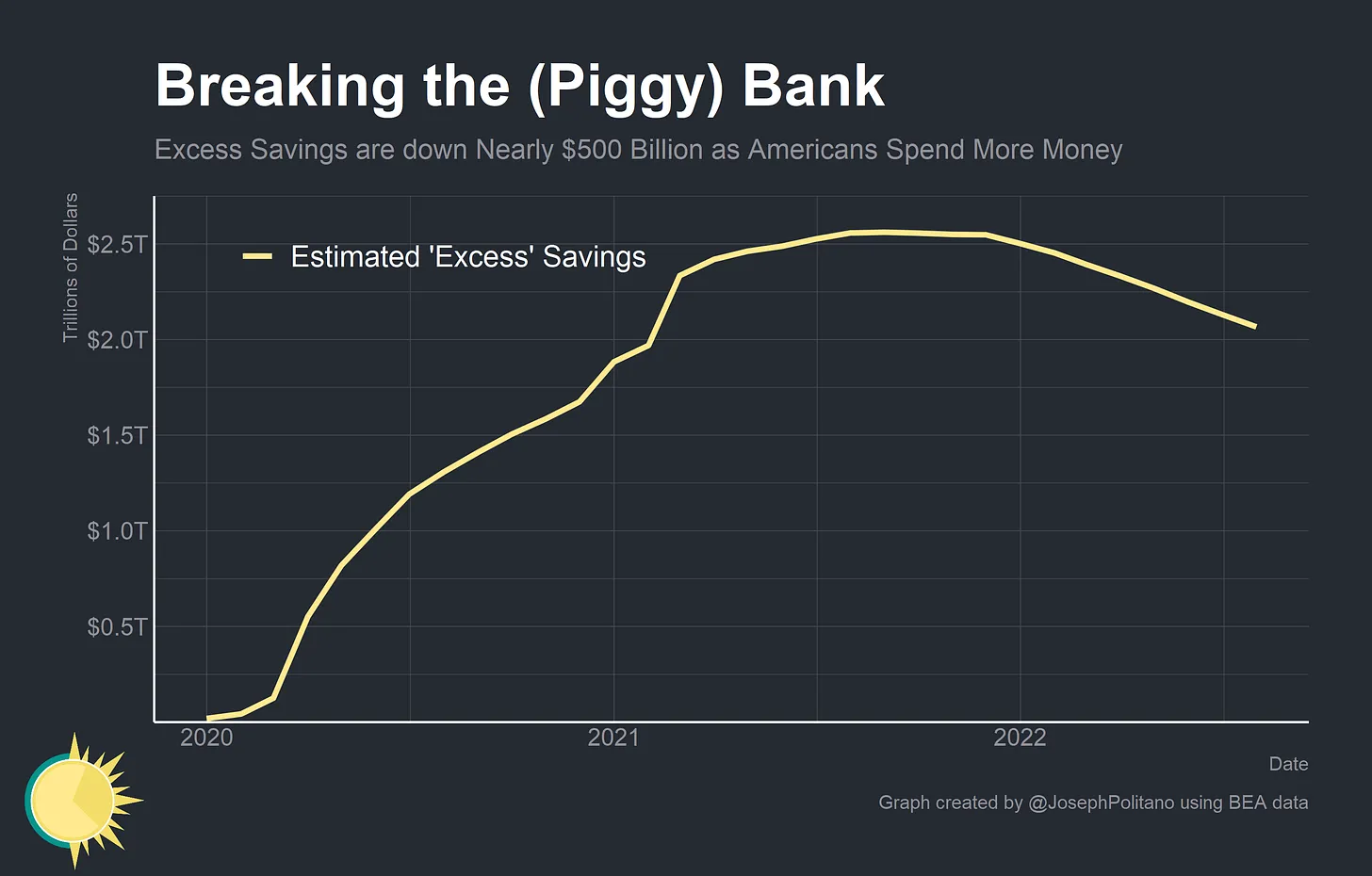

Another part of the problem is that Americans saved a yachtload of money from 2020-late 2021 (tons of government relief + not being able to go anywhere will do that for you)… and have spent the last year collectively spending down their savings.

Until inflation cools off, the Fed plans to keep jacking up interest rates, which is increasing everyone’s fears that we’ll be stuck in a haunted house full of still-high prices, higher unemployment, and costly borrowing, maybe all at the same time.

Look for the bear necessities

We are officially in a “bear” market, which, to most people, means that a major market index like the S&P 500 or the Dow has dropped 20% from recent highs. In fairness, we were due for a correction; for a good long while, markets have been like my seven-year-old after a fistful of Sour Patch Kids and a Marvel movie (i.e., way too excited and overconfident). History (and Bloomberg.com) says we’ve still got a ways to go before we hit true bottom, which (on average) takes 15-16 months and a 38% dip.

The origins of “bear” and his optimistic brother “bull” to describe markets are apocryphal at best (pioneer fur traders? what is this, Oregon Trail??). Some sources attribute the term to how bears attack by swiping down at their prey, versus bulls tending to charge and gore upward.

My own guess as to the etymology of “bear market” before I looked into it was a bit cozier and way less macabre. I thought about how bears behave in winter: their activity drops. When bears sense winter coming, they create a secure little den, build a tremendous reserve of saved-up energy, and dramatically slow themselves down.

And that, I think, is what we should all do too! But with our money, instead of salmon and berries and naps (although that does sound wonderful, so do some of that too if you want).

Rather than panic-selling (don’t do that!) and doomscrolling, it’s time to make like a bear and focus on what we can do to prepare for financial winter. The short list:

- Reinforce your household’s income streams.

- Be intentional about your optional spending.

- Build your emergency savings.

- Pay down your high-risk debts, and avoid taking on new ones.

- Review your estate plan and insurance mix.

- Invest more—if you have all your ducks in a row.

- Look for ways to be generous.

- Filter your inputs.

How to bear up under pressure

What, exactly, is a financially-savvy, thoughtful, and really quite charming person to do? (That’s you.) Take a deep breath, tune out the news, and focus on the things that are within your control. It’s not a coincidence that these are all valid suggestions whether the economy is up or down—effective financial strategies are trend-resistant.

Reinforce your household’s income streams.

Although recessions don’t always include job losses and high unemployment, different industries will likely feel the pain of economic backslides in different ways. Shoring up and diversifying your income streams now will put you on firmer footing later if your employer chooses to cut hours or jobs.

Reinforcing your income might mean keeping and excelling at your current job (including asking for a raise, if your company is doing well and you’re a high performer). It might mean taking advantage of the many vacancies in the job market and looking for a place to work that gives you back some money, time, or sanity (ideally all three).

If you’ve got the bandwidth, improving your income streams might mean adding a side hustle or passive income generator. If you’ve already got a hobby that you love, you could monetize what you make. If you’re highly skilled or knowledgeable at something useful, you can take a low-risk approach and offer to team up with an established business to make, teach, or write something that they need.

It’s also a good time to look for cost-effective ways to skill up, whether in something related to your primary job or in a field you’d like to join. Now is not a good time to borrow money for more education… but free, employer-paid, and self-paid-and-in-your-budget training and education is a great idea.

Be intentional about your optional spending.

Intentionally spending for joy—using your money to support your well-being, interpersonal connection, and pleasure in lasting ways—looks different for everybody. Put some thought into what it means for you. I’m advocating for intentionality, not asceticism. It is essential to nurture your joy and care for your whole self, and that doesn’t have to mean expensive purchases or activities. Look carefully at the effect you’re trying to achieve, and try to identify whether there’s an equally meaningful and more affordable way to create that positive effect.

Seasonal decor is a great example. It can be easy to get sucked into spending $100 on new stuff to celebrate the change of the seasons… but you could also check out a low-cost, low-effort guide to cozy fall decor like this one or this one (both from The Nester, queen of cozy minimalism), and create an equally positive emotional effect for a much smaller outlay.

Look for places where you can pause or dial down spending that isn’t necessary or particularly joyful for you, and really enjoy the hell out of your fun money when you do spend it.

We’ve got some simple and ultra-low-cost self-care suggestions that are aimed at actually helping you feel better when everything is on fire, retail therapy not required.

Build your emergency savings.

This is something we recommend regardless of season, but when financial winter is coming, we definitely want to make like a bear and fortify ourselves to outlast a season of scarcity.

If you have no savings yet, try to save up a single paycheck or $1000, whichever is lower. Our long-term recommendation for an emergency fund is 6-12 months of expenses (more on that here and here). If you’re already saving for retirement but don’t yet have an emergency fund, we recommend you pause retirement contributions and prioritize stockpiling liquid cash until you have at least three months’ expenses in a high-yield savings account. And you should check on your tax withholdings to make sure you’re not waiting til next year to get money you may need now.

Pay down your high-risk debts, and avoid taking on new ones.

Getting rid of your debts might sound like a low-priority, pie-in-the-sky, “someday I should do that, but certainly not NOW” goal. But hear me out.

If you lose your job or your hours get cut (both of which are increasingly likely in recession conditions), or something else happens that hurts your income, you might not be able to make your payments. If you aren’t able to make your payments, you’re paying late fees, accruing interest, and facing hits to your credit score… or even repossession or foreclosure. All of that obviously has a long-term impact on your financial future. Knocking out as many ankle-biter debts as possible will add to your short-term margin of safety.

We personally like the snowball method of debt prioritization, but it’s not just about what works for us; you’ll be most motivated by what makes sense for you. And in high-stress times, maybe you feel most motivated to focus on highest-risk debts first. This isn’t necessarily about amount or interest rate (although both are a factor)… it’s about getting rid of things that have the highest potential to hurt your big picture, and ideally, that can free up more of your purchasing power. The highest-risk debts for most people are unsecured loans (except student loans only while interest and payments are paused, currently through December 31, 2022), credit cards, retirement account loans, and upside-down auto loans.

If you’re still not sure how to prioritize your paydown (or why you would even want to do that), book a free Financial Strategy Session and I’ll help you figure it out.

Review your estate plan and insurance mix.

This is big-picture thinking… but hey, so is catastrophizing about the possibility of a recession over which you have no control! Why not make the gloomy vibes work for you by planning for kinda-grim-but-very-important items?

- Create or update your will, financial power of attorney, and healthcare power of attorney.

- Look into short term/long term disability insurance (STD/LTD), which covers you in the event that you cannot work. We don’t love all “opt-in” employer benefits (increasingly, those seem to just be insurance sales disguised as HR), but STD/LTD coverage through your employer is often a good call if they offer it.

- Evaluate your need for term life insurance (not whole life) if anyone depends on your income.

- Audit your healthcare spending (and get everyone in your household a checkup) so you’re ready to make changes when open enrollment kicks off on November 1.

Invest more—if you have all your ducks in a row.

When the market’s down 20%, that means stocks are on sale! You can add to your retirement investing if you haven’t yet met your contribution limits and you don’t anticipate needing the funds before you’re 60. If you’re a parent, you can save for kids’ college in a 529 or ESA, or you can open a non-tax-favored brokerage account. Remember: it’s really, really important to save for emergencies or time-sensitive priorities (like, “I need a new car next year” or “I want to buy a house in 3 years”) outside of the market, especially if we’re in for a bumpy ride.

Our general guidelines for any type of investing:

- eliminate your non-mortgage debt (or, at a minimum, your high risk debts as described above)

- have at least 3 months’ expenses in a dedicated emergency fund in a HYSA

- don’t invest money you may need within the next five years

- if you’re not sure where to start, use our 10/10/1 rule: look for index funds that have been open for at least 10 years, with 10% returns over the life of the fund, and fees (a.k.a. expense ratios or loads) of less than 1%. I just pulled up 18 funds on Fidelity’s research tool that meet those criteria, even in this economy!

Look for ways to be generous.

Going into a season of scarcity, it can be surprisingly helpful to consider ways (even small ways) to be generous with your resources. Generosity tells us we’ve got enough to share and connects us to our community. Sharing your time or talent or resources, even just a little, switches off the part of our brains that keep saying “Oh no, there isn’t enough!” We create a little cognitive dissonance when we commit a generous act despite feeling a bit scarce. Our brain says “Wait, maybe there IS enough! Look, we’re sharing! Things must be better than we thought!”

We’ve shared tips on building a generosity practice here. In our experience, a committed practice of being generous with your time, money, or resources can be a great tool to help with feelings of powerlessness, overwhelm, and fear.

Filter your inputs.

It’s been said that you are the average of the five people you spend the most time with—and it’s also been said that you’re actually influenced by a far larger number than five (your friends’ friends can affect you pretty powerfully too). And those are just the people you know! Most of us let the ideas of total strangers tap-dance through the hallowed halls of our minds all the time (e.g., podcasts, Instagram, newscasts, Facebook, books, TikTok, old-school paper newspapers, email newsletters, entertaining-yet-informative personal finance websites…).

Many of these resources use algorithms that serve us more of what we already seem to like, so we’re getting lots of repetition and reinforcement. The algorithms also serve us things that keep our eyeballs glued to our glowboxes for as long as possible, because that’s how they monetize us. (Remember, friends: if the app or website is free to use, that’s because YOU are the product. Usually because your attention is being sold to advertisers.) This can be problematic, because what keeps our attention is often stuff that promotes powerful emotional responses. I say all of this to point out what you probably already know: there’s a possibility that some of the things in your mind palace aren’t helpful, beautiful things that you intentionally put there.

If you’re feeling depressed or anxious about the state of the world, that’s not an unreasonable response to an unceasing barrage of negative information. And there are always plenty of advertisers (and influencers pushing spon-con) trying to get you to buy things that will supposedly make you feel better! Even without “treat yo’self” self-care advertising, emotional spending is a thing. It’s incredibly common for most of us to try and use some financial power to make up for feeling powerless. But there’s real power in deciding what you’re allowing to influence your well-being or your financial life.

So… if you want… take a very gentle and curious look at the things you read and watch, and see if any of them deserve an unpaid vacation. Mute, unfollow, unsubscribe, uninstall, and delete anything that isn’t actually making you feel good about yourself, your life, and the world. Just for a little while. I promise it will all still be there if you miss it.

That’s it! That’s the list! Now, it’s your turn. What strategies, tricks, and (hopefully healthy) coping mechanisms are helping you deal with financial stress? Let us know here or drop us a line, and don’t hesitate to reach out if you need some support.

one more bear, as your reward for reading to the end. bye!

Header photo credit: Pixabay on Pexels.com

Leave a comment