Whether you follow financial news or just regular news, you’re probably hearing a lot about inflation and interest rate hikes. There’s a good chance this is the first real time you’ve seen inflation in your financial life. If you were born after 1981, it’s the first time in your actual life that inflation has been this high.

If you’ve forgotten what inflation really means (and at this point you’re too afraid to ask), I got you. This is long, so here’s a little tl;dr for my time-pressed readers:

- Inflation is the overall change in how much it costs an imaginary average urban American to live their life. A little bit of inflation (2-2.5% over a year) is normal and good; right now we’re seeing more like 8-9%, and that’s stressing everyone out.

- Inflation has spiked because we have seen big increases in demand (people’s desire + ability to pay for things)… coupled with decreases in supply (the availability of the goods and services that consumers want).

- The government wants to keep inflation at that 2-2.5% level. Their biggest tool to do so is to raise interest rates, which ultimately encourages consumers to spend less and save more, cooling down demand and (eventually) prices.

- As an individual consumer, the smart play right now is to pay down debt and save more so you don’t have to borrow as much in the future. We know this is no small feat when everything costs more, but we’re going to be stuck in this spot for a little while. Do what you can to get more comfortable.

- If you’re ready to start investing (which we define as “free of non-mortgage debt, with at least 3 months of expenses in savings, + surplus income to invest”)… don’t be spooked by turbulent markets. Stocks are on sale, baby!

- We put money that we won’t need for at least five years into passively managed index funds.

- We pick funds with at least 10 years of data (preferably more like 20) showing average annual returns over 8% (preferably over 10%), with fees less than 1% (preferably much, much lower).

If you want to know more about any of the above (and you know you do), read on!

How the US measures inflation

The most popular measure of inflation comes from something called the “Consumer Price Index,” which is based on an imaginary urban consumer’s monthly spending “market basket” of over 80,000 goods, services, utilities, fees, tolls and some other types of taxes. (The CPI also studies rent prices, but because rents change more slowly, this data is captured every six months.) The information about what goes in the basket comes from government survey data, and the prices come from in-person, phone, and online price checks.

Changes in the total cost of this “basket of goods” from month-to-month and year-to-year tell us how much inflation the US is seeing.

Let’s acknowledge some limitations: the CPI is not perfect. It doesn’t include rural areas (although urban-area consumers make up ~93% of the US population, so it does cover a lot of ground). The CPI weights things internally based on averages that might have little to do with you. For example, the basket is weighted with the assumption that people eat more chicken than tofu. This might be true at large, but not if you’re a committed vegetarian.

The designation “urban” also includes a huge range of costs of living, but it isn’t always easy to see what’s happening in your individual area (you can try here!). The overall CPI number paints a picture of the whole country, but New York and San Francisco are very different from Charlotte or Birmingham or Tampa or Richmond. Recent analysis from one of my favorite newsletters, The Morning Brew, notes that the South and Southwest have seen overall higher inflation rates than other parts of the country.

- Shameless plug: I sincerely love The Morning Brew and many of its affiliated letters, which keep me up-to-date on all the latest financial news. Please sign up through my referral link if you want to get smarter about money and business while laughing. (This recommendation is unpaid, but their referral program earns you fun swag.)

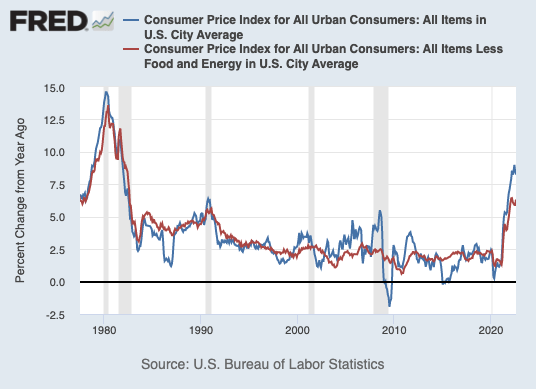

The CPI as a gauge of inflation lets you measure the difference between the total cost of the market basket at different points in time. When you see a report that “year-over-year inflation was 8.3%,” that means that the whole market basket costs 8.3% more than it did one year ago.

There’s also a thing called “core inflation.” This excludes the prices of the ever-changeable food and energy sectors, and so it tends to be far, far more stable. After a couple decades of relative stability, core inflation is also way up 6.3% year-over-year.

So while food and energy are driving a lot of inflation, it’s not just food and energy – it’s everything. Clothes, medical goods and services (like doctor visits and prescription drugs), recreation, vices (like alcohol and tobacco), housing, and cars and other transportation are all showing big changes, too. And sustained, widespread inflationary trends like these are usually the ones that prompt the government to take action.

Why is inflation so crazy right now?

The current situation, in some ways, is a pretty solid illustration of Econ 101 “supply and demand” concepts that you might remember from back in the day.

First of all, there are lots of things (both goods and services) that are in shorter supply. This is for a whole pile of reasons, like viruses and wars, and the resulting supply chain problems and labor and manufacturing shortages. This scarcity also comes from super huge changes in the types of things that many people wanted to buy, all happening within a very short period of time – trading gym memberships for home exercise equipment, and work pants for sweatpants (and then back again).

As things become increasingly scarce, it’s natural for businesses to adjust prices higher for their remaining stock/availability, since they won’t be able to turn a profit on sold-out products. Then, businesses eventually reach a tipping point where they start to lose customers, and prices tend to stop going up.

Car sales over the last few years show this trend pretty clearly. Pre-pandemic, it was really unusual for car dealers to charge more than MSRP (Manufacturer Suggested Retail Price) for new cars. Post-March 2020, the supply of new cars grew really short (thanks to shipping delays and manufacturing problems with critical parts like microchips). But consumers still wanted cars, so dealerships could tack on all kinds of crazy new fees for the few cars they did have, and consumers would cough up the cash, even if they weren’t happy about it. (Ford and GM have been cracking down on a variety of overcharging behaviors, in large part because their brands are taking the hit for customer dissatisfaction.)

At the same time as the supply of lots of necessary and/or desirable goods and services went down, the demand for many of those things also went way up. This is, again, because of super huge lifestyle changes affecting numerous people and the things they wanted to buy in a short period of time (e.g., “I can’t get on a plane to go on vacation, so I’ll just buy a nice new car and drive someplace!”). The government also instituted a number of economic relief programs aimed at helping people (and companies) keep more dollars in their pocket to weather the pandemic-related storms.

People having more money in their pockets, and fewer avenues to spend it, increased customer willingness to throw money around in hard-to-predict ways. Wages went up a bit as well, which also helped support the increase in demand. But a majority of Americans are now worried that their income won’t keep up with inflation.

Continued out-of-control inflation is generally agreed to be a terrible thing, especially for poor people and people on fixed incomes. Because of this, and also because many people vote based on what they believe will help their wallet, the government has opened their (slightly dusty) toolbox.

The government starts taking an interest

Say hi to the Fed. (Full name: the Federal Reserve System, whose job is – among other things – keeping the U.S. economy on a smooth and stable course and optimizing employment.)

If inflation goes up too fast, the Fed raises “interest rates.” This doesn’t mean that they are directly raising interest on consumer financial products like your credit card or mortgage. The Fed has the power to change the “federal funds rate,” which (in simplified terms) is kind of like the interest earned by giant savings accounts that commercial banks keep with the government, and the interest rate that these banks pay to borrow money from each other.

For two years (since March 2020), the federal funds rate had been hovering slightly above 0%, offering economic relief for companies’ and consumers’ pandemic-induced pains. When the federal funds rate is low, it becomes less rewarding to hoard money, and far easier (and cheaper) to borrow money. Low interest rates were a gift to many consumers struggling to make ends meet thanks to pandemic-related un- and under-employment, but that’s ultimately part of why demand got out so far ahead of supply; these low rates made it much easier to spend money.

In March 2022, the Fed started dialing things back up, and up, and up. The reason the Fed is raising interest rates is, ultimately, to incentivize people (and companies) to spend less money, borrow less money, and save more money. If the federal funds rate goes up, banks earn more by leaving their money where it is. They also pay more to borrow money. Banks then pass those earnings and costs on to their customers, the people and companies saving with and borrowing from the banks.

The government’s hope is that a shift away from borrow-and-spend and towards wait-and-save will dial down the high demand that’s been pushing up prices. A drop in demand will normally encourage companies to cut their prices, which will lower the total price of that big basket o’goods… thus cooling off inflation and (hopefully) getting the economy back in a stable place.

If this all sounds too theoretical, let’s say you live in an area with a hot housing market (yes, I realize that means almost anywhere). You can probably see this already happening with housing prices. People were house-shopping like crazy when mortgage rates were under 3 percent: buying homes sight unseen, waiving inspections, and bidding $50k over asking. It didn’t hurt that plenty of people were tired of their homes after quarantine, and that tons of people from pricey cities started relocating to mid-priced cities, driving up demand in numerous markets. Investors also joined the fray, buying up single-family houses to convert to rentals. This drove up home prices and rent. (There are early signs that the investor frenzy may be cooling off a little.)

Even in optimal conditions (let alone amid historic supply-chain disruptions and labor shortages), it’s hard to just magically make new single-family houses happen quickly. Thus, housing supply in many cities got incredibly short. Enterprising home sellers said “I can jack up my selling price like crazy and these suckers will still pay it!” But thanks to the increase in mortgage rates… things have changed.

Now that mortgage rates are back over 6%, plenty of people are instead responding “actually, I’m gonna stay put for awhile and save up a bigger down payment while I wait for the market to cool off. Brb, googling how to sell a kidney.” And in some places, this is starting to slow down the housing craze! (A little. Maybe not enough for my friends’ and clients’ stress levels and homebuyer hopes.)

When the Fed raises interest rates, they are hoping to trigger that kind of slowdown everywhere. This will ideally prompt vendors to cut prices, and bring year-over-year inflation back down to a nice steady 2-2.5%.

What does this mean for me?

We’re all thinking it, so I’m just gonna say it: for most of us, this does not feel great. We’ve been living in a low-interest, low-inflation world. Financially speaking, that tends to feel pretty good! But for now, those days are coming to a close.

In the near term, it will become more expensive to borrow money, and it will (probably slowly) become more rewarding to save money. If all goes well, a slowdown in spending will cool down prices, and a serious inflation-driven economic crisis will be averted.

Still, you may not feel great stuck between the rock of high prices and the hard place of high interest rates. So what’s a human to do?

Some will probably say that it’s smarter to hold on to your debts right now. After all, who knows when you’ll be able to borrow money that cheaply again? But overall, we at Fortuna Money are still advocates for paying off your non-mortgage debts so you can reclaim your purchasing power.

The reason we’re so passionate about eliminating non-mortgage debts is simple: it gives you options. The $200 or $500 or $1000 a month that was going towards credit cards or a car payment or a loan is no longer spoken for – it’s back in the game, and it can help you shore up your financial future.

You can use that money to build an emergency fund, so you won’t have to put the next HVAC repair on your credit card. You can use it to save in advance for your next car, so a big down payment can keep your future car payment really small. (Or you could even save enough to pay cash for that future car!) You can use it to increase your retirement contributions or open a brokerage account. You can use it to get a credential that qualifies you for a raise at work.

And if you pay down your non-mortgage debts, that can help your credit score. If you borrow money again in a higher-interest future world, an improved score can help you qualify for better rates than you might get if you kept all your old debts around.

If you’re still not sold, remember: paying down your debts early saves you interest in a way that is effectively the same as you earning that interest rate. If you pay down the loan that’s currently charging you 10% interest, that ultimately does the same thing for your net worth as investing someplace that guarantees that you earn 10% interest.

I don’t know about you, but I would take a guaranteed 10% return in a heartbeat.

One last question: do interest and inflation have anything to do with the markets tanking?

Yes. Interest rates going up – in multiple countries worldwide at the same time, because the US of A is not the only place feeling this pain – are a big part of why the markets are so spooked.

The very thing that is trying to help consumers, calming down wildly high prices, is striking fear in the hearts of major shareholders. Maybe because it’s going to cut into their exponential earnings. Maybe because they’re concerned that these rate hikes will have major ripple effects: consumers spend less, so vendors cut prices, but then vendors make less money, so vendors lay off people, and unemployed consumers spend even less; repeat until the heat death of the universe.

This fear isn’t completely illogical, but it’s incredibly shortsighted. We don’t need that kind of energy here.

Regular investors sometimes see this panic happening and, urged by increasingly hysterical news headlines, they get on the bandwagon and lock in their losses by selling low.

But that’s not going to be you, dear reader. Because you’re not a regular investor, you’re a cool investor.

You aren’t scared of market downturns because you built a solid emergency fund before you started investing. And you definitely didn’t put any money in the markets that you’d need within the next five years. To you, a market downturn is simply an opportunity to buy stocks at a discount.

Cool investors recognize that even if the markets are having a rough year…

They’re still way up over the last five years…

And way, way up over the last 40 years.

Cool investors know that the markets are a long-term win, even if they avoid checking their 401(k) balances when everyone else is freaking out.

The bottom line here: don’t panic.

Even if these things were undeniable signs of a painful recession (which is still far from certain, with a ridiculously strong labor market and calming consumer sentiment)… it’s not time to panic. It’s time to focus on the things that are within your personal power. Inflation and interest rates and markets are outside your sphere of control (unless you’re on the Federal Reserve board of governors, in which case, hello and thank you for stopping by).

Your income streams, your optional spending, and your saving and debt decisions are far more significant to your personal well-being than the zigs and zags of inflation and interest rates. Take charge of those things now as much as possible, and make financial decisions with a slightly pessimistic eye towards the future. Assume your holiday bonus this year might be the Jelly-of-the-Month club, and don’t put 50% down on the new pool just yet.

Focus on making choices that grow your income, stabilize your spending, and boost your net worth, and you’ll be better prepared to ride out any bumpy stretches that are yet to come. If you’d like help figuring out how to insulate your specific financial situation against these turbulent times, book a Financial Strategy Session today… because we’re here to help you manage your money and your stress levels.

Photo credits – Header: Monstera on Pexels.com, Basket: Darya Makshanova on Pexels.com, S&P 500 trends: Google Finance’s Market Summary tool.

[…] the holidays, you might still be unhappy in your personal relationship with the economy. Thanks to major inflation (a.k.a. price increases) and interest rate hikes hitting Americans right in the wallet, the vibes have been off for awhile. The markets are a […]

LikeLike