We got a great question this week from a friend of ours who is both an airline pilot and an Air National Guard member, and after diving into the research, I’d thought I’d share it with you. Even if you’re not a pilot or a servicemember, you might bump up against this issue if you change jobs and wind up contributing to multiple retirement plans in the same year.

Most employer-provided retirement plans are qualified retirement plans, which are tax-favored plans set up by employers; this includes 401(k), 403(b), SEP, SIMPLE, and profit-sharing plans. Military and government employees have access to a special qualified retirement plan called the Thrift Savings Plan (TSP). Because all of these accounts have tax implications for the employee and for the employer, there are rules that you won’t want to break.

The question

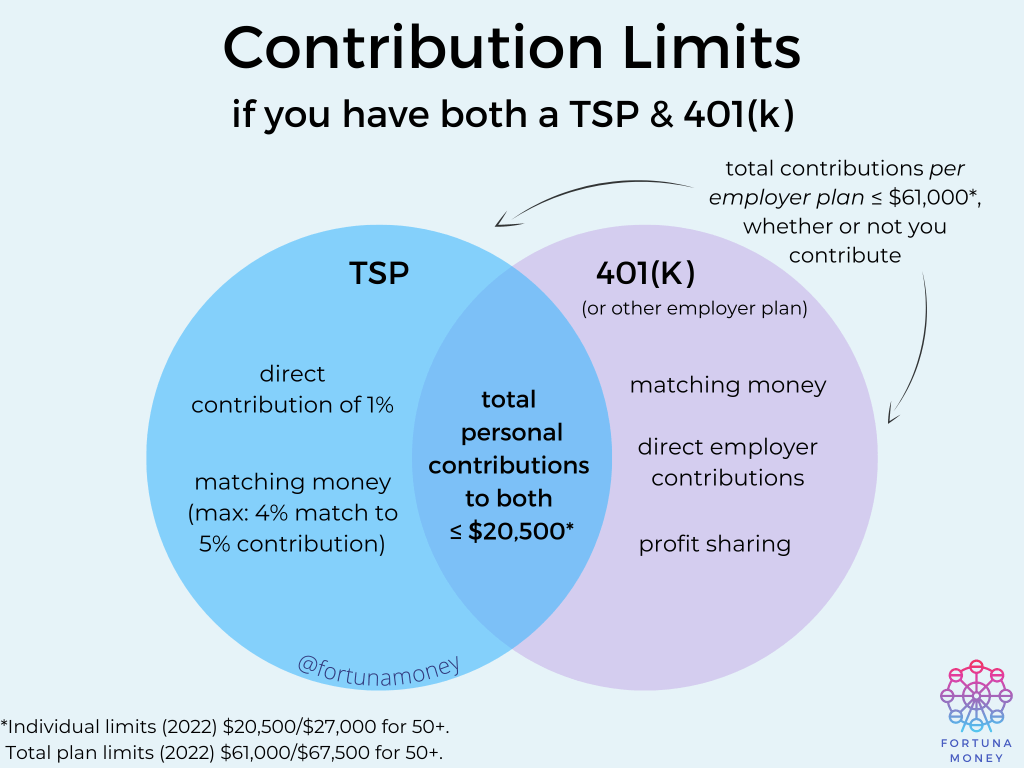

If you have both a Thrift Savings Plan and a 401(k) option, or more than one TSP/401(k), are you allowed to max out the personal contribution limit in each account? Or is your limit the total of all your personal contributions?

The answer

Your personal contribution max # is your cumulative total for the year across all qualified retirement plans. This amount is per person, so if you’re married, your 401(k)/TSP contributions are not affected by your spouse’s individual 401(k)/TSP contributions. The max personal contribution is $20,500 in 2022 (or $27,000 if you’re over 50 and eligible for “catch-up” contributions)… no matter how many different employer accounts you’ve contributed to.

The IRS doesn’t care about how many different places you work; they care about your total wages that year, and whether you’ve paid enough taxes on those. The IRS doesn’t think of your TSP and your 401(k) as different pots of money. When they bust out their special IRS blacklight, all they see is one single pile of bright, glowing, not-yet-taxed income, and that pile had better not be too big or the taxman cometh.

But wait, there’s more! And this is where it gets weird (or awesome, if you’re lucky enough for it to apply to you): if your employer makes matching and/or direct contributions to your 401(k), the overall contribution limit per retirement plan per employer is quite a bit higher. That’s right: with a little help from your employer, the total contributions for the year to that employer’s retirement plan can be up to $61,000 ($67,500 for 50+), inclusive of any contributions you make. That’s right — this upper limit includes your personal contributions to that employer’s plan. So keep in mind that if you contribute the personal max of $20,500, your employer can’t contribute more than $40,500 through matching, direct, and/or profit-sharing contributions.

Mr. Fortuna and I had a fun debate about the edge case of how much the highest-paid government employee could bank in their TSP in a given year. Turns out, the top-paid guy is a Veterans Health Administration medical officer making $464,227 per year x 5% = $23,213. He’d be capped at the personal max, so the most he’d sock away would be $41,000.

So, mathematically, you can’t get $61K in your TSP. The good news: it doesn’t affect your overall max in another plan.

If you left that job in the same year for another generous magical unicorn employer, you could theoretically get ANOTHER $61,000 from that second employer, but your personal contributions would still be cumulative. (The reason the employer limit isn’t cumulative appears to be because those direct contributions count towards the employer’s tax deduction, not yours.)

And now for a useful hypothetical, specific to any dual-hatted airline pilot/military members out there: several of the major airlines currently make a direct contribution of 16% to their pilots’ 401(k)s. A pilot making $381,250 and getting that 16% direct contribution would max out the total employer plan contribution of $61,000. Therefore, it would be smartest to make sure all personal contributions (of up to $20,500) went into their TSP, where they could take advantage of the up-to-5% match. You can slide the scale according to what makes the most sense for you — just make sure your total personal contributions across all employer plans don’t exceed $20,500 ($27,000 if you’re over 50).

What’s the worst that could happen?

If you accidentally contribute too much, it can trigger paperwork and an unexpected tax bill (or even — yikes — double taxation). It’s nothing irreversible, but the earlier you fix it, the better. There are more details and some helpful examples of what this can look like for TSP holders here. If you think there’s any chance you might be in the danger zone this year, talk to a tax professional ASAP — it’s much easier to fix this issue ahead of time if you can.

What about my other retirement accounts?

One final clarifying note: all of these limits are specific to qualified retirement plans — again, those are tax-favored plans set up by employers. Individually-opened traditional IRAs and Roth IRAs are also tax-favored but in different ways. If I start talking at length about those, this post will quadruple in size. But because I don’t want to leave you hanging, here’s the quick and dirty:

- The combined annual contribution limit for both traditional and Roth IRAs is $6000 ($7000 for 50+). It’s fine to contribute to each, as long as your total contributions aren’t more than that across all IRAs.

- Contributions to a Roth IRA are taxed at the starting line (i.e. you fund them with money that’s already had taxes withheld) and are not tax-deductible. You get to take out the contributions and the earnings tax-free at the finish line (i.e., after retirement).

- Roth IRAs have income limits. To make a full contribution, your household needs at least that much earned income in a given tax year. If you’re single and making more than $129K, or married and making more than $204K, you will need to dive into your tax return (and possibly call a tax pro) to figure out how much you’re allowed to contribute directly to a Roth in that tax year, and what you can do as a workaround if needed.

- Contributions to a traditional IRA can be tax-deductible in the year that you make them; the contributions and earnings are taxed at the finish line.

- Traditional IRAs do not have income limits; however, the tax benefit does phase out based on your income. It’s also impacted by your marital/filing status and if anyone in your household is contributing to an employer retirement plan like a 401(k); you can find more information on those limits here. If you’re single and making over $68,000 or married and your household is making over $109,000, check and see how your possible tax deduction may be affected by the other elements of your situation.

Header photo by Karolina Grabowska on Pexels.com.