The audio version of this post can be found here.

I fought budgeting tooth and nail.

Kind of embarrassing to admit it now that I’m a financial coach, but there it is.

Something about the idea of living on a budget sounded WAY too much like the idea of living on a finicky, exhausting calorie-counting diet. I have worked way too hard to heal my teenage issues around food and my body to count calories now, and the idea of applying that kind of restrictive calculus to spending kicked up some serious rage against the adding machine. I was also, as I’ve mentioned elsewhere, the spendy, blithe “free spirit” to my husband’s oversaver-”nerd,” and it sounded an awful lot like he was trying to ruin my fun.

But somehow, probably because Mr. Fortuna has the patience of a saint and because I do ultimately believe in things like math, I came around. A big part of what worked for me was when it finally hit me that creating a budget meant I was writing “permission slips” for myself to spend without guilt (from myself or from the nerd beloved husband). It didn’t mean I could say “yes” to myself all the time, but it did mean that I got to fully enjoy those “yeses” without feeling anxious. We also realized together that a good budget gives a job to every dollar that comes into your life, while also allowing room to purposefully “re-task” those dollars when life happens.

Mr. Fortuna thinks we should actually go so far as to stop calling it a “budget” and start calling it a “spending plan,” and I’m not gonna lie, I kinda like that. To go back to the food analogy, it’s a lot more like changing your lifestyle to be generally healthier, while allowing yourself to have treats on a designated “cheat day” without feeling bad about it.

I tell people that it usually takes about three months to really build your budgeting muscles, and after that, it becomes more or less second nature. Unfortunately, what that also means is that I’m a few years removed from the best ways to get over the initial hump of budgeting adaptation.

Lucky for me, I have some amazing friends who are also very financially savvy. One particularly awesome independent woman, Whitney, began budgeting about 18 months ago. In that time she has seen her net worth increase by 110% of her base salary, thanks to a combination of extremely thoughtful money management and nonstop hustle. One of Whitney’s side gigs is creating these lovely and incredibly unique handmade “prayer cards” — check more examples out here on Etsy.

We met over warm caffeinated beverages, and Whitney was generous enough to share some great thoughts for this post. She even left her 2020 budget planner with me for an inside look at how she managed to pull off her impressive financial reversal. Here are some of the things we talked about:

- Come up with categories that fit the way YOU spend. One of the hardest things about starting to budget is figuring out what percentage you are “supposed” to spend on different things (to say nothing of knowing whether you should calculate based on net or gross). Here’s the deal: a one-size-fits-all recommendation doesn’t usually fit anyone perfectly. Instead, get curious about what actually is happening in your money. Look back at your spending over the last couple of months – and if you’re not in acute financial distress, Whitney even recommends taking a month where you spend exactly how you want to, and then reviewing to see where your money really wants to go on its own. After that, you may realize that the categories that work for everyone else don’t make that much sense for you. For example, plenty of people might categorize all restaurant expenses as “food,” but Whitney realized she considered going out with friends on the weekends to be part of her “entertainment” spending, and so that’s how she categorizes it – which totally works!

- Get over your fear of money. This is a big one, especially if you grew up with weird family attitudes about money — and let’s be honest, most of us did (it’s not our parents’ fault; they did their best).

Money is not inherently evil. Money is just a tool. Like a hammer, it can be used to break a window or build a house. And like the aliens in that War of the Worlds movie, money is much scarier before you actually get a good look at it. Once you know your net worth — your assets and debts — and your income and expenses, your money becomes a solvable paper-and-pencil (or spreadsheet/app) problem not much more emotionally complicated than measuring a spot in your house for a new bookshelf. The question becomes “does what I want fit here?” without any judgments directed at the bookshelf or your house — or yourself. Avoidance is a totally understandable emotional response that’s been trying to protect you from stress, but it’s not serving you anymore. And along with that…

- Get over your fear of talking about money. Start sharing with a small number of people you can fully trust, who will support you and encourage you. You’re not a bad person if you care about money or want to become wealthy. You’re not greedy if you want to be paid a fair market value for your job. You’re not dumb because you’ve got debt. And you’re not “in bad taste” for talking about any of this with people you trust.

Carefully selecting a small group of people who are financially thoughtful and supportive of your goals can supercharge your progress. It can also keep you engaged and accountable. (I’d be remiss if I didn’t mention that one of those people could totally be me, your friendly neighborhood financial coach.)

People who are excited about your journey may also start looking for ways to help you out, whether it’s connecting you with a job opportunity, sharing news about your side hustle, or tipping you off to a better living situation.

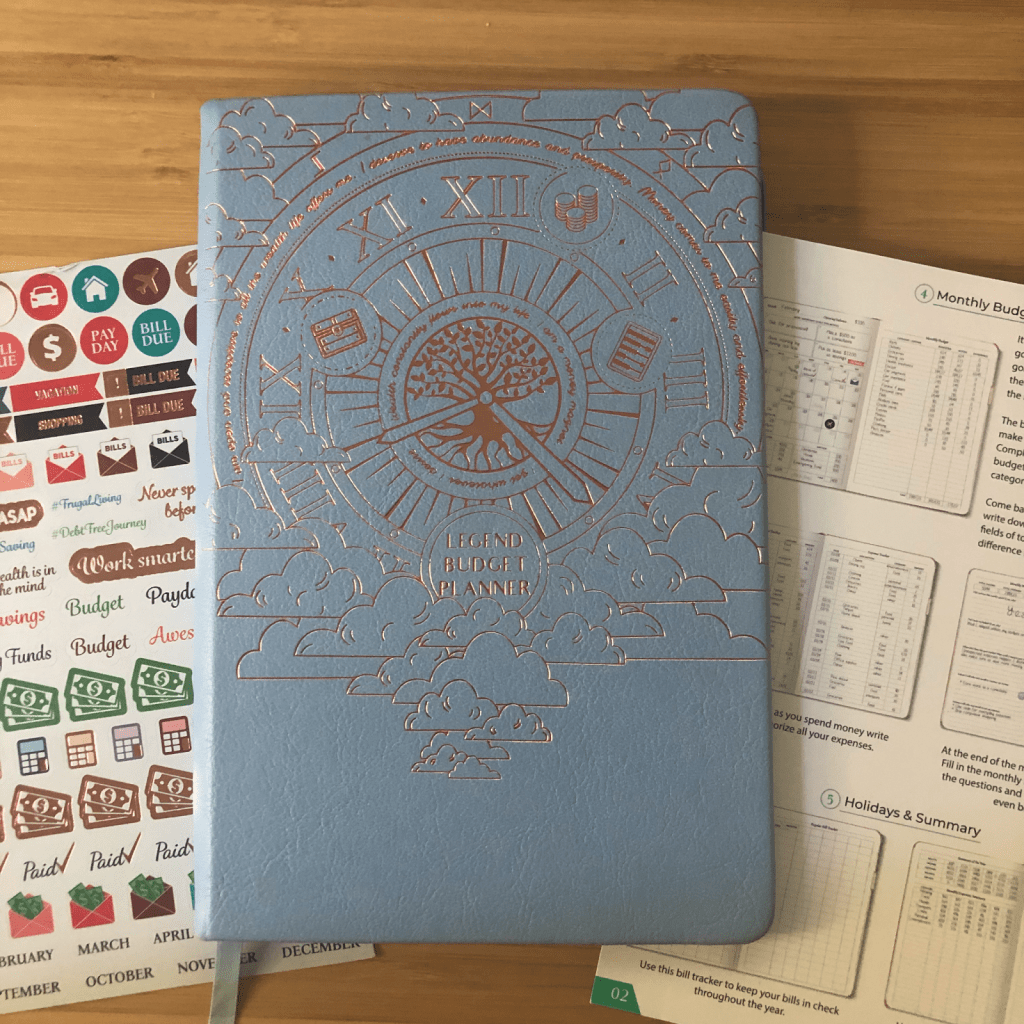

- Find the right tool. Whitney’s favorite was the Legend Budget Planner (shown above, available here and here with even more color options), and judging by her organizational skills and delightful handwriting, this was a great fit — so if you’re a journal kind of person, check it out. It’s undated and has monthly goal-setting and end-of-month reviews for both financial and emotional reflections. There are also a lot of people who are very happy using Excel or Google Sheets for daily budget maintenance.

I have said before that we use Mint, and automation has been absolutely key to winning with money for me. I like a spreadsheet as much as (ok, more than) the next girl, especially for long-term planning, but I’m not wired for the kind of consistency required for daily DIY budgeting (e.g., a written planner or spreadsheet). Even if I don’t feel like writing down and categorizing my transactions every day, Mint will keep an eye on all of my accounts and I can catch up when it’s convenient instead of getting overwhelmed and giving up. I have also heard outstanding things about YNAB.

We’re planning a roundup of some of the major budgeting apps in a future post; in the meantime, just know that however your brain works, there really is a tool out there that can help you make your budget as simplified or as detailed as you want. On a related note, you could always…

- Try giving yourself a “per diem” for ALL expenses outside of fixed categories. I love this one so much because it gives you a ton of flexibility in a really simple container. Once you’ve figured out how much money needs to go towards truly fixed expenses — baseline food costs, housing, utilities, transportation — you can then calculate how much you can afford to give yourself for an “average daily spend.” You can customize this in a way that supports your individual situation. Whitney’s “per diem” allowed her to go out to lunch if she wanted to, and also incentivized her to pick cheaper restaurants or pack a lunch if she wanted to go out with friends over the weekend.

This reminds me of a great strategy in Get Good With Money, a truly essential personal finance read from the incomparable Tiffany Aliche (aka “The Budgetnista”). She helps you break down your expenses into the truly fixed (“B” for bills, like housing costs), the fixed-but-a-little-flexible (“UB” for utility bills, like electricity), and the highly-flexible (pretty much everything else is in “C” for cash). The Budgetnista says that if your B+UB costs dominate your budget, you may have an income issue, and if your C expenses comprise too big a chunk, you may be an overspender. You should read her book for more details, but all of this is to say: if you find yourself in the “potential overspender” category, you could take the “per diem” approach for your “C” expenses to help yourself get a handle on your controllable spending costs.

- Set 1 appointment a week to do the “business” of being you. This was Whitney’s suggestion, and I think it’s especially essential if you’re doing your money solo. Put it on the calendar and treat it like a real appointment. The Budgetnista also recommends that you make it as pleasant as possible — put on music and pour yourself something tasty to drink — and the psychology major in me appreciates the value of a little positive reinforcement when building good habits.

In our house we usually have a budget meeting about three times a month these days — once at the beginning to set it, once in the middle to evaluate and course-correct where needed, and once at the end to ratchet down any spare dollars and put them towards our fun money and goals. My husband learned a few years ago that springing a budget meeting on me when I’m in the middle of a project or have just snuggled under the covers with a novel goes over about as well as a turd in a punchbowl. So whether you’re budgeting on your own or with a partner, find a time of day where everyone involved is alert, unhurried, and in a relatively good mood. And maybe bring snacks.

- Take non-spending “sabbaths.” Whitney recommends these as a form of resistance against consumer culture, and I love it. I tend to make no-spend pledges when I see that I’ve been spending a lot on a particular category of things, or if I know I need to use up my backstock before I treat myself to more, but I’ve also considered a more radical approach. Thus far I’ve had a couple of Sephora no-spend seasons, as well as a plant purchase sabbath. (Mr. Fortuna believes I have too many plants. I respectfully disagree.) I have yet to try a true long-haul no-spend, but if a spending sabbath of any length appeals to you (or just sounds baffling enough that you want to know more), I really loved Cait Flanders’s The Year of Less.

These big-picture strategies may help you get over any initial resistance to working on your budget spending plan. If you still feel like you might need some support to get over the hump, hit me up.

The Amazon links in this post are affiliate links, which means that if you choose to make a purchase through the links, the price is the same for you, and Fortuna will a) get a small commission from Amazon’s Affiliate program and b) be super grateful for your click!

Love the reframe of budget vs “spending plan”. I’m def going to use that more encouraging terminology from now on! I think I’ll start using “turd in a punch bowl” more often too. Hahaha. Great article—thank you!

LikeLiked by 1 person

[…] I’m going to tell you that you need a spending plan. At minimum, you need to know how much you spend in an average month. If you’ve already paid off […]

LikeLike